Introduction

Combine large, bold images with the beautifully crafted words of your story.

Introduction

Why predicted OTA domination never occurred

Expedia and Travelocity both turned 27 this year.

Back in 1996, their birth announcements were often reported concurrently with an obituary for traditional travel agencies.

The 2023 Travel Weekly Travel Industry Survey provides the clearest picture yet why that death knell was rung prematurely.

According to the doomsayers, technology was supposed to spell the end of the era of human travel retailing. But it turned out that, to counter the threat from OTAs, different technologies were developed to allow advisors to be both independent and home-based, reducing overhead costs significantly and enabling them to stay competitive. The survey shows that 72% of all advisors identify as independent, with the majority of those working from their homes.

These technologies were primarily developed and deployed at scale by hosts and consortia. Another piece of the story falls into place when you see how widespread membership in these organizations are: According to the survey, a significant majority of advisors are hosted or belong to a consortium.

But that’s still not the full story. The lowering of overhead and the efficiencies that booking technologies provided would not have been enough if suppliers felt that the online channel could truly take care of their needs. After all, the OTAs’ scale and global reach is so advantageous that they occupy three of the top 10 slots in the 2023 Travel Weekly Power List, including Nos. 1 and 2.

OTAs, however, tend to dominate in areas where travel products are, essentially, commodities. If a hotel room is available through multiple OTAs, online shoppers simply buy where the price is lowest. And if they’re all the same price, they’ll go wherever they belong to a loyalty program.

Advisors thrive today because an important segment of travel is not commoditized. And this year’s Travel Industry Survey shows that the most successful advisors lean into those areas that require a more bespoke approach. They court clients who appreciate their advice and service.

Who are those clients? Brands often cite that courting young travelers is a key to maximizing the value of a customer over a lifetime. But brand loyalty tends to get diluted over time as new brands tailored to changing times enter the scene.

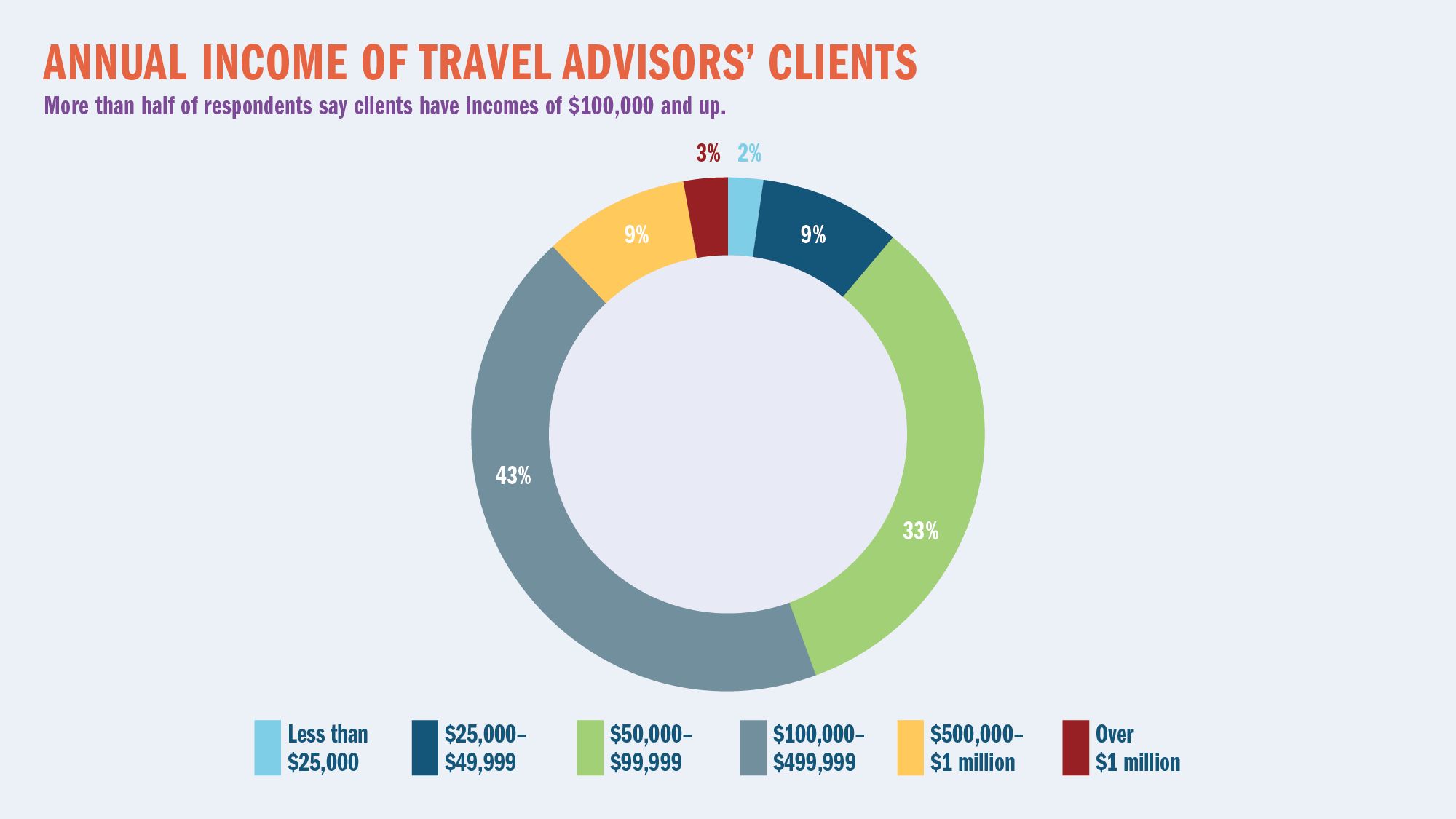

Millennials and Gen Z travelers certainly use travel advisors, but the survey shows advisors disproportionately target clients who are older and wealthier than the average traveler and who have more time and money to travel. Seventy-two percent of travel advisor clients are over 40, and 55% have an annual income of $100,000 or above (see chart above).

Along the same lines, it becomes clear in the survey that it’s in suppliers’ self-interest to provide attention and support to advisors. Whereas OTAs shout about how much money they’re saving clients, the travel advisor clientele isn’t looking for a bargain.

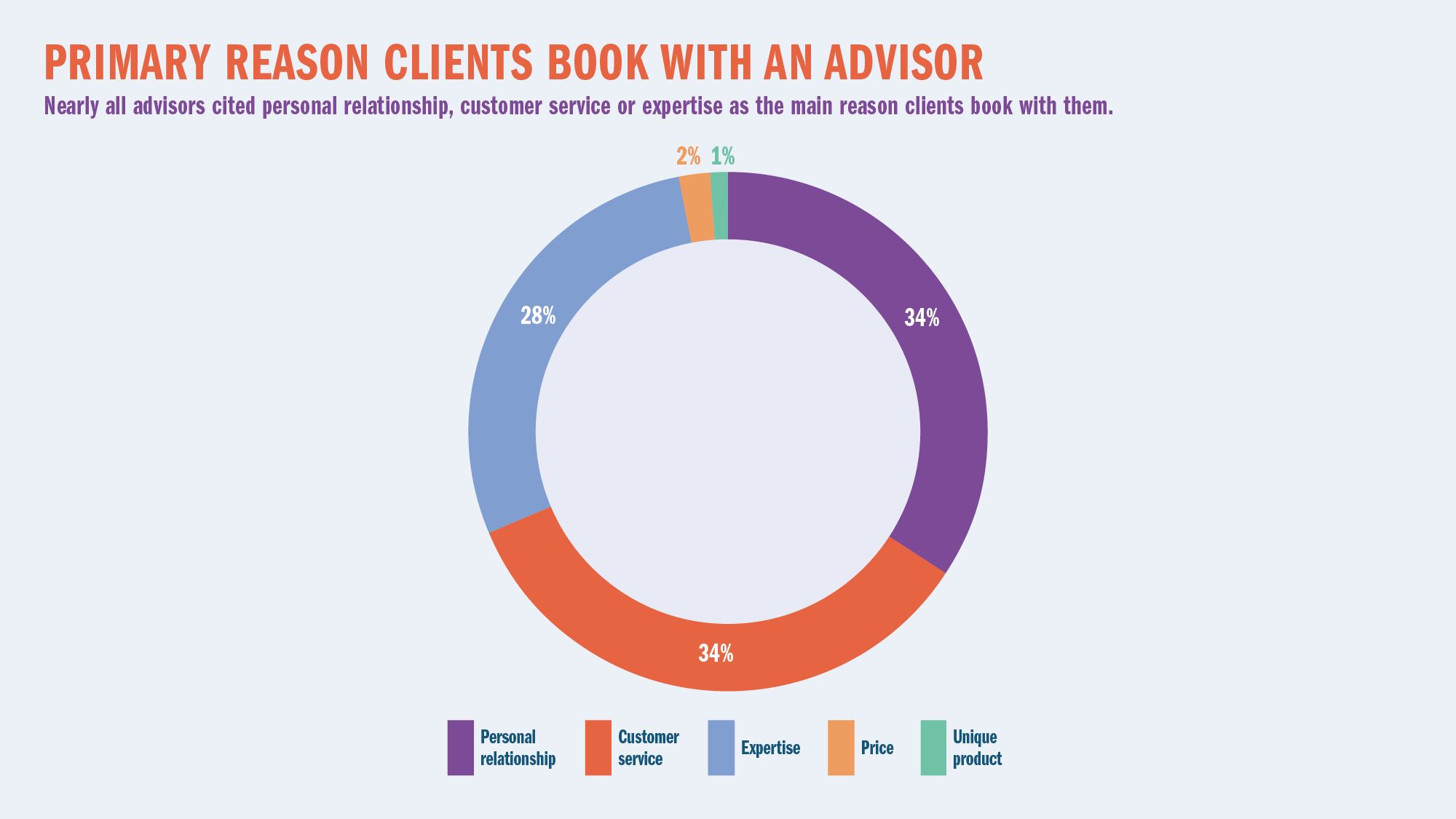

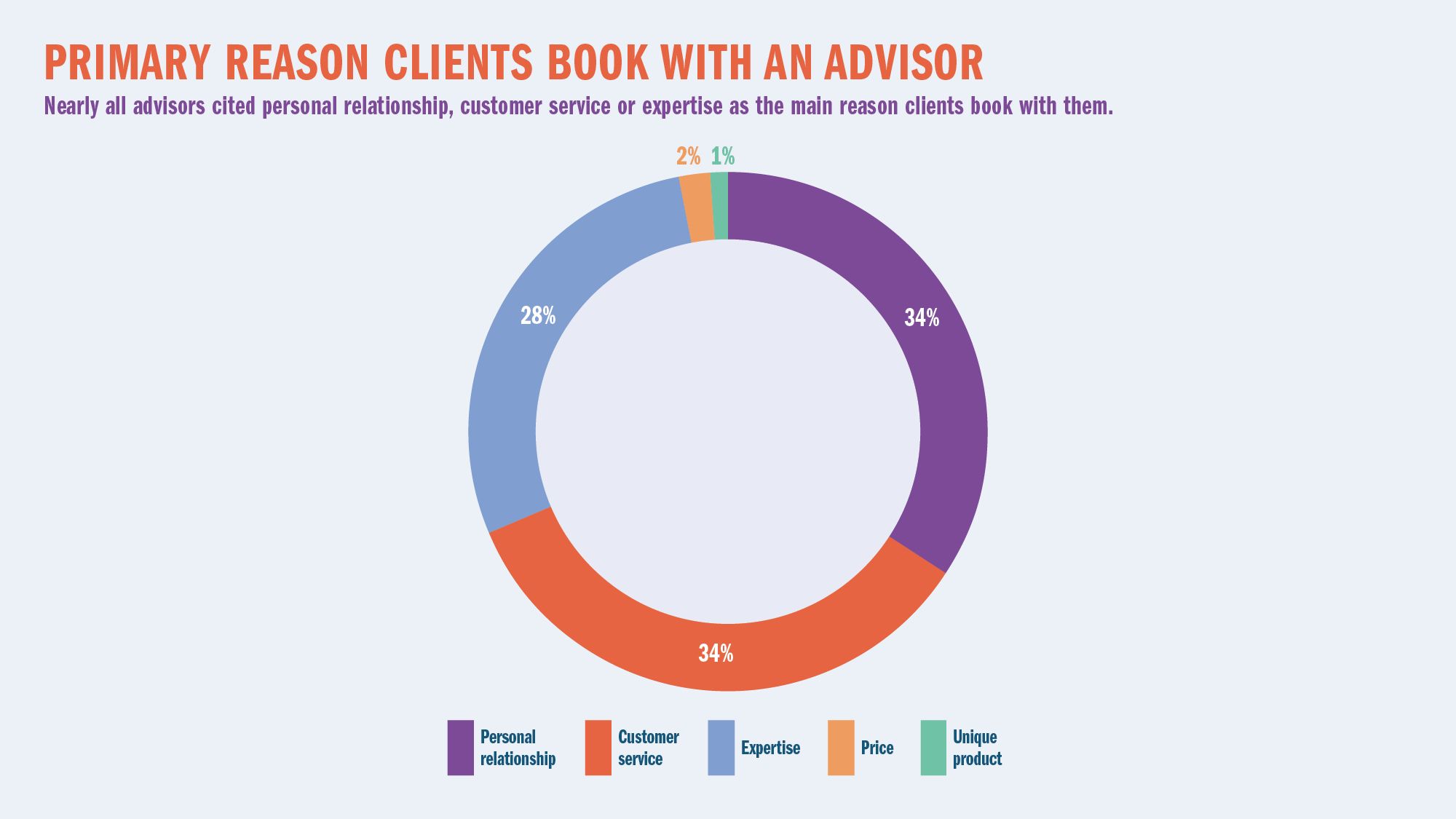

In fact, according to the survey, the development of a relationship drives 34% of clients to use an advisor, their reputation for service drives another 34% and 28% go to an advisor for their expertise. Only 2% contact a travel advisor because they’re looking for a deal. It’s only natural that suppliers would reward distribution channels commensurate with their profitability, and they know that travel advisors provide them with their highest margins.

Charles Darwin’s theories are often misrepresented by the phrase “survival of the fittest.” In fact, what he observed was that a successful species isn’t necessarily the one that’s biggest or strongest, it’s the one that successfully adapts to changing conditions. The proof of travel advisors’ ability to successfully adapt — to evolve — are detailed in the charts, graphs and commentary you’re about to read.

Arnie Weissmann

Executive Vice President and Editor in Chief, Travel Weekly